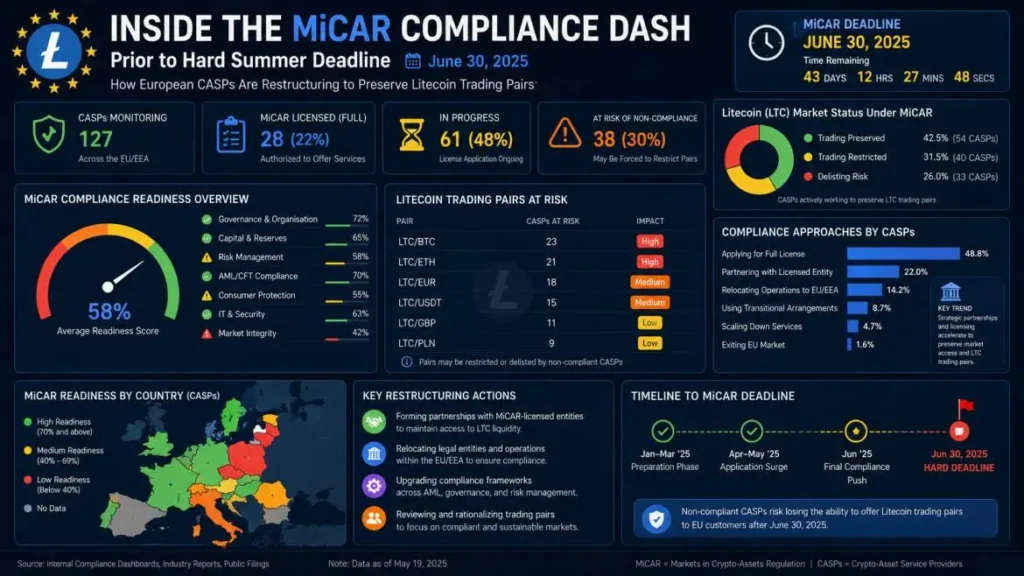

Inside the MiCAR Compliance Dash Prior to Hard Summer Deadline: How European CASPs Are Restructuring to Preserve Litecoin Trading Pairs

The European digital asset ecosystem has reached its structural turning point. Following the European Securities and Markets Authority (ESMA) updated regulatory briefings released on April 17, 2026, the digital financial sector is locked in a high-stakes MiCAR Compliance Dash Prior to Hard Summer Deadline. ESMA has confirmed that the transitional grandfathering grace period under Article 143(3) of the Markets in Crypto-Assets Regulation (MiCAR) will definitively end on July 1, 2026.

After this date, any Virtual Asset Service Provider (VASP) operating under legacy national exemptions must hold a full Crypto Asset Service Provider (CASP) authorization or immediately trigger an operational wind-down.

This regulatory shift has triggered an intense operational scramble for platforms hosting decentralized assets. Because Litecoin (LTC) is structurally categorized as a decentralized commodity without an identifiable single issuer, European CASPs have focused heavily on structuring their compliance, passporting, and custody models. Their objective is clear: safely maintain deep LTC trading pairs ahead of the upcoming hard stop without assuming catastrophic legal liabilities.

The July 1, 2026 Cliff: Anatomy of the Regulatory Hard Stop

The transitional arrangements provided under MiCAR gave member states the discretion to allow existing VASPs to continue providing services for up to 18 months after the December 30, 2024 implementation date. However, this fragmented approach resulted in an uneven playing field. While jurisdictions like Germany (BaFin) and Ireland shortened this runway, nations like France (AMF) and Luxembourg (CSSF) maintained the full 18-month grandfathering window.

The April 2026 ESMA clarification has eliminated any remaining regulatory ambiguity, mandating a coordinated, absolute enforcement baseline across all National Competent Authorities (NCAs) by July 1, 2026.

| Member State Jurisdiction | Original VASP Regime | Grandfathering Duration Expiry | Status for Unlicensed Firms Post-July 1, 2026 |

| France (AMF) | PSAN (Registered) | July 1, 2026 | Immediate Service Cessation & Offboarding |

| Luxembourg (CSSF) | VASP Registration | July 1, 2026 | Mandatory Execution of Operational Wind-Down |

| Germany (BaFin) | Crypto Custody Licence | Dec 31, 2025 (Expired) | Already Integrated into National CASP Standard |

| Ireland (CBI) | VASP Framework | Dec 30, 2025 (Expired) | Already Integrated into National CASP Standard |

| Spain (CNMV) | VASP Registry | Dec 30, 2025 (Expired) | Already Integrated into National CASP Standard |

For compliance teams, the ending of this grace period removes the ability to operate across border lines via bilateral national agreements. Any entity providing crypto-asset services to EU citizens without a validated Title V CASP licence post-deadline will face severe administrative fines, asset freezes, and market-abuse enforcement actions. This reality has concentrated institutional attention on legacy liquidity pools—specifically older, established assets like Litecoin that lack centralized corporate or foundational support structures to handle regulatory overhead.

The No-Issuer Conundrum: Categorizing Litecoin Under the MiCAR Compliance Dash Prior to Hard Summer Deadline

A central challenge within the current compliance dash centers on asset classification and its associated disclosure requirements. Under MiCAR Title II, any crypto-asset offered to the public or admitted to trading must have an aligned crypto-asset whitepaper. For standard utility tokens or foundation-backed layer-1 networks, this requirement follows a predictable path: the issuing entity drafts the document, notifies its home NCA, and assumes statutory liability for its accuracy.

Litecoin presents a unique structural problem. It is a pure, decentralized, proof-of-work protocol derived from the Bitcoin source code. It has no centralized foundation that exercises control, no official corporate management, and no single issuer. Under Article 4 of MiCAR, when an asset lacks an identifiable single issuer, the responsibility and the legal liability for creating, notifying, and maintaining the crypto-asset whitepaper shifts entirely to the CASP that operates the trading platform.

Key Regulatory Axiom: Under MiCAR, if you operate an order-matching engine and admit an issuerless asset to trading, your entity assumes the legal fiction of the “offerer.” You are legally liable for any material misstatements, omissions, or non-compliance contained within that asset’s whitepaper.

To address this challenge, European digital asset platforms are employing several key legal strategies:

- Consortium Whitepaper Drafting: Top-tier European exchanges are creating compliance consortia to pool legal costs and share the analytical burden of drafting standardized whitepapers for issuerless commodities like LTC.

- Indemnification Restructuring: Platforms are revising their terms of service to clearly state the structural limits of their technical assessments, isolating their corporate balance sheets from consumer class-action lawsuits regarding protocol-level changes (such as code forks or network upgrades).

- Prudential Capital Safeguarding: Compliance officers are increasing their capital reserves to handle potential liability claims under Article 4.

To quantify this operational risk, institutions use a specialized formula to calculate capital reserves $C_{cap}$ for listing issuerless commodities:

$$C_{cap} = \max\left(V_{min}, \quad \alpha \cdot \sum_{i=1}^{n} L_{i} \cdot \sigma_{i}\right)$$

Where $V_{min}$ represents the statutory minimum capital required by Article 67, $L_{i}$ represents the nominal trading volume of the issuerless asset $i$, $\sigma_{i}$ represents the annualized volatility index of that specific asset, and $\alpha$ is the scaling risk coefficient determined by the local NCA.

Passporting Fractures: Upgrading National VASP Registrations

The core economic advantage of obtaining a full MiCAR CASP licence is the European passporting framework. Under legacy VASP registrations, an exchange authorized in Paris could not freely market its services or acquire clients in Rome or Frankfurt without separate, time-consuming applications to individual NCAs.

The migration process from a local VASP registration to a unified CASP model is complex. It requires an operational upgrade across three key functional layers:

Operational Resilience and Governance

Firms must prove that their senior management meets strict fitness and propriety criteria. This includes clean regulatory track records, formal certifications in digital financial risk management, and physical presence within the chosen EU home member state.

Anti-Money Laundering (AML) and Counter-Disaster Financing (CFT) Implementation

Legacy VASP models frequently utilized simplified due diligence for low-volume retail accounts. The fully realized MiCAR standard requires complete implementation of the EU Transfer of Funds Regulation (TFR) alongside advanced transaction monitoring. This involves real-time blockchain analytics capable of tracking the ultimate beneficial ownership of incoming assets, even when routed through sophisticated unhosted wallet infrastructures.

Cross-Border NCA Notification Protocols

Once a home NCA (such as the French AMF or the Maltese MFSA) grants an official CASP license, the provider must submit an explicit cross-border passporting notification under Article 63. This notification must detail every member state the platform intends to target, its operational architecture, and the specific languages its marketing materials will utilize.

The local NCA has a limited 30-day window to transfer this information to host-country regulators and ESMA’s central registry, making early application submissions vital to preventing service interruptions.

Operational Architecture: Restructuring Custody and Liquidity Layers

The most complex technical shifts occurring during this compliance push are found within the operational custody layers governed by Article 75. The updated ESMA briefings from April 2026 explicitly target third-country outsourcing arrangements. Many European exchanges historically relied on non-EU entities—specifically liquidity hubs and institutional custodians based in the United States, Switzerland, or Asian jurisdictions—to clear trades and custody client assets.

ESMA’s updated guidance clarifies that a CASP cannot outsource its primary custody operations to unauthorized non-EU entities if that outsourcing effectively bypasses MiCAR supervision. This restriction has broken established order routing and liquidity loops.

[Legacy Non-Compliant Architecture]

EU Client -> EU VASP Front-End -> Third-Country Custodian (US/Asia) -> Non-EU Liquidity Hub

[Compliant 2026 Architecture]

EU Client -> Authorized EU CASP -> Segregated MiCAR Wallet (EU Soil) -> Compliant Liquidity Router

To maintain deep LTC trading pairs under this framework, compliance and engineering teams are restructuring their execution stacks around three core operational pillars:

On-Shoring Custody Nodes

Firms are migrating their cryptographic key-management systems to legal entities physically located within the EU. This involves implementing multi-signature and Multi-Party Computation (MPC) architectures where the controlling nodes reside on secure server infrastructure within EEA borders, ensuring compliance with Article 75’s strict asset isolation mandates.

Bifurcation of Order Book Liquidity

To manage international liquidity constraints without violating market abuse regulations, European platforms are establishing ring-fenced order books. For example, an LTC/EUR pair must settle completely on-chain or via internal ledgers managed by fully authorized EU entities.

If a platform routes overflow orders to foreign market makers, those market makers must enter the system as regulated entities or clear their trades through an intermediary EU clearing house.

Upgrading Liquidity Provision Agreements

Existing market-making contracts are being re-negotiated to embed real-time trade transparency constraints. Market makers must guarantee that their quoting engines comply with MiCAR’s pre-trade and post-trade transparency rules, including printing trade logs to public feeds within fractional timeframes.

Institutional Cost-Benefit Analysis: The LTC Trade-Off

Operating a compliant trading venue under 2026 standards requires ongoing capital and operational investment. Platforms must balance the expenses associated with maintaining issuerless token whitepapers against the economic benefits of retaining established proof-of-work asset pairs.

Comprehensive Institutional Evaluation Matrix

Pros

- Retaining Market Share: Litecoin remains a highly liquid payment commodity with consistent transactional throughput. Maintaining these pairs prevents users from migrating to offshore platforms or non-compliant alternative venues.

- Fee Generation Resilience: Because LTC trading pairs exhibit predictable volume patterns across different liquidity cycles, they offer consistent fee generation that can help offset the overhead costs of compliance monitoring.

- Reduced Protocol Counterparty Risk: Unlike complex smart-contract platforms or decentralized finance (DeFi) governance tokens, Litecoin’s codebase is structurally stable. This minimizes the risk of sudden code exploits, governance attacks, or protocol-level compliance failures.

Cons

- Direct Whitepaper Liability Exposure: The CASP assumes full civil and corporate liability for the Title II disclosure requirements, exposing the business to legal action if an unforeseen protocol vulnerability impacts retail consumers.

- Increased Regulatory Audit Overhead: Local NCAs require ongoing tracking of network centralization metrics, distribution profiles, and mining power concentration to confirm the asset remains fully decentralized.

- Capital Lock-Up Costs: Maintaining issuerless pairs requires higher capital allocations under internal risk formulas, reducing the capital efficiency of the platform’s broader corporate balance sheet.

The Enforcement Blueprint: What Happens on July 2, 2026?

When the clock strikes midnight on July 1, 2026, the regulatory grace period ends. The enforcement strategy mapped out by ESMA and national regulators is designed to identify and penalize non-compliant operators swiftly.

[July 1, 2026: Grandfathering Ends]

│

├──► [Authorised CASPs]: Initiate seamless cross-border passporting.

│

└──► [Unauthorised VASPs]: Must execute formal wind-down protocols.

│

├──► Cease trading pairs.

├──► Offboard EU retail users.

└──► Transfer assets to self-hosted/licensed vaults.

If an unauthorized platform continues to facilitate trades on July 2, 2026, regulators will execute a multi-tier enforcement process:

- Immediate Cease-and-Desist Demands: NCAs will issue public notices forcing the targeted platform to freeze trading pairs for EU citizens and stop all marketing operations.

- Structural Administrative Fines: Regulators can levy substantial financial penalties. For corporate entities, these fines can reach up to 12.5% of their total annual global turnover from the preceding financial year.

- Mandatory Client Migration Execution: Non-compliant platforms will be legally required to transfer client funds to authorized, licensed third-party CASPs or facilitate a full migration to verifiable self-hosted wallets, with all associated transaction fees absorbed by the failing firm.

This strict enforcement design emphasizes the importance of the current compliance push. For European digital asset firms, upgrading to the MiCAR standard is no longer a long-term strategic goal—it is an immediate operational necessity required to maintain business continuity, protect consumer access, and survive the impending regulatory shift.

FAQ SECTION

-What is the exact deadline for the MiCAR transitional grace period?

- The final transitional grandfathering grace period under Article 143(3) of MiCAR officially expires on July 1, 2026. After this date, all digital asset service providers operating within the European Union must have a fully validated CASP license or cease their consumer-facing operations.

-Why does Litecoin pose a unique compliance challenge under MiCAR?

- Litecoin is a decentralized proof-of-work asset without an identifiable corporate or foundational issuer. Under MiCAR Title II, because there is no central issuer to draft and submit the mandatory crypto-asset whitepaper, the legal responsibility and liability for this documentation shifts entirely to the CASPs listing the asset.

-Can European exchanges outsource asset custody to US-based custodians after July 2026?

- According to the April 17, 2026 ESMA statement, outsourcing core asset custody to non-EU third-country entities that are not bound by MiCAR supervision is heavily restricted. CASPs must maintain primary control over cryptographic keys within authorized EU legal entities to comply with Article 75.

-What are the financial penalties for operating without a CASP licence after the deadline?

- NCAs are authorized to apply significant administrative sanctions. Non-compliant corporate platforms can face fines up to 12.5% of their total annual global turnover, public censure, asset freezes, and potential criminal prosecution of their executive officers.

-How does MiCAR passporting work for newly authorized CASPs?

- Once an operator receives full CASP authorization from its home country NCA, it submits a notification detailing its target markets under Article 63. The home regulator has 30 days to inform host-country regulators and ESMA, allowing the platform to passport its services across all 27 EU member states seamlessly.

FINANCIAL DISCLAIMER

Financial Disclaimer: This analytical publication is provided strictly for informational and educational purposes. It does not constitute legal, compliance, financial, investment, or operational advice. The regulatory landscape governing digital assets is subject to swift change and varied enforcement interpretations by National Competent Authorities (NCAs). Readers should consult qualified legal counsels and regulatory compliance experts to evaluate specific operational strategies under the Markets in Crypto-Assets Regulation (MiCAR).