Institutional Spotlights on XRPL Cross-Border Settlement Utilities: Resolving the Dual-Leg Problem in Real-Time Wholesale Finance

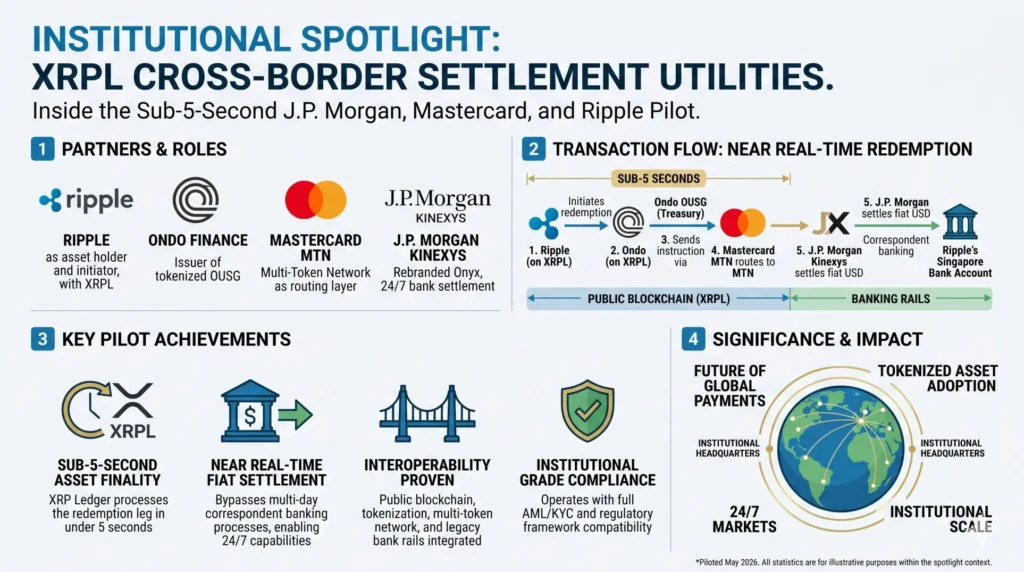

Institutional Spotlights on XRPL Cross-Border Settlement Utilities have taken center stage in the wake of market updates published on May 12, 2026. Financial reports confirmed a successful joint live pilot involving Ondo Finance, J.P. Morgan’s Kinexys platform, Mastercard, and Ripple. The operation achieved what legacy financial infrastructure has long struggled to deliver: a near-real-time cross-border redemption of a tokenized U.S. Treasury fund, clearing the public blockchain asset leg in under five seconds and executing the corresponding fiat settlement across international borders outside standard banking hours.

This pilot demonstrates a framework where public layer-1 ledgers, multi-token messaging layers, and global systemically important bank (G-SIB) rails function in tandem. By orchestrating a unified workflow between the XRP Ledger (XRPL), Mastercard’s Multi-Token Network (MTN), and Kinexys by J.P. Morgan, the participating entities have established a functional blueprint for the 24/7/365 movement of wholesale institutional capital.

The Mechanics of the Sub-Five-Second Cross-Border Redemption

The core technical achievement of the May 2026 pilot lies in solving the “dual-leg problem.” In typical real-world asset (RWA) tokenization models, the digital asset leg settles instantly on-chain, but the corresponding cash or fiat leg remains bound to legacy settlement cycles (T+1 to T+3) via traditional clearing houses and correspondent banks. This misalignment generates counterparty risk, ties up capital, and demands manual, siloed reconciliation.

The pilot established an automated bridge across these environments. The transaction structure progressed through four distinct phases:

- On-Chain Initiation: Ripple, acting as an institutional participant holding Ondo Short-Term U.S. Government Treasuries (OUSG) tokens on the XRPL, initiated a partial redemption of its holdings. The asset leg settled on the public XRPL infrastructure in under five seconds. The payout asset utilized was Ripple’s U.S. dollar-pegged stablecoin, RLUSD, which operates under New York State Department of Financial Services (NY DFS) regulatory oversight.

- Interoperability Handover: Upon verification of the on-chain redemption, Ondo Finance generated a fiat payout instruction. Rather than routing this manually, the instruction was transmitted through the Mastercard Multi-Token Network (MTN). The MTN served as a programmable interoperability layer, translating the blockchain-native state change into a verified financial instruction compatible with institutional banking protocols.

- Ledger Synchronization: The Mastercard MTN routed the instructions directly to Kinexys by J.P. Morgan. Kinexys, the rebranded evolution of J.P. Morgan’s Onyx blockchain unit, automatically debited Ondo Finance’s Blockchain Deposit Account held at the bank.

- Wholesale Settlement Finality: Kinexys transferred the corresponding fiat USD proceeds into Ripple’s commercial bank account in Singapore via J.P. Morgan’s established correspondent banking network. The transaction was completed entirely outside standard banking hours, providing Ripple with accessible liquidity before traditional markets opened.

+------------------------------------------------------------------------+

| THE DUAL-LEG SETTLEMENT FLOW |

+------------------------------------------------------------------------+

| |

| [ RIPPLE ] --- (Redeems OUSG Assets via RLUSD Stablecoin) |

| | |

| v |

| [ XRP LEDGER ] --- (Finalizes Public Blockchain Leg < 5 Seconds) |

| | |

| v |

| [ ONDO FINANCE ] --- (Issues Automated Payout Instruction) |

| | |

| v |

| [ MASTERCARD MTN ] --- (Translates & Routes Cross-Network Message) |

| | |

| v |

| [ J.P. MORGAN KINEXYS ] --- (Debits Ondo's Blockchain Deposit Acct) |

| | |

| v |

| [ CORRESPONDENT RAILS ] --- (Credits Fiat USD to Singapore Account) |

| |

+------------------------------------------------------------------------+Macro Dynamics Driving Institutional Spotlights on XRPL Cross-Border Settlement Utilities

The momentum surrounding this architecture is tied directly to broader macro shifts in corporate treasury demands, central bank interest rate policies, and evolving regulatory boundaries.

Capital Efficiency and Treasury Opportunity Costs

With U.S. Treasury yields remaining structurally significant, the opportunity cost of idle capital has forced corporate treasurers to reconsider liquidity management. Traditional cross-border wire transfers that stall over weekends or during market closures constrain capital.

By utilizing tokenized versions of short-term treasuries (such as OUSG, which is backed by institutional vehicles like BlackRock’s BUIDL fund), entities can continuously earn yield on their reserve assets while retaining the capability to redeem them into actionable fiat liquidity within minutes.

The Role of Regulated Public-Private Stablecoins

A critical element of this pilot’s success is the use of RLUSD for the initial public blockchain settlement leg. Historically, Tier-1 financial institutions avoided relying on highly volatile public native assets like XRP or ETH for wholesale corporate cash management due to slippage risks and strict balance sheet accounting rules.

The integration of an NY DFS-regulated stablecoin offers a compliant, dollar-denominated settlement instrument that matches the underlying speed of the XRPL without exposing institutional balance sheets to asset-liability mismatches.

Interbank Ecosystem Proliferation

J.P. Morgan’s commitment to public-private hybrid networks is evident in its filing for products like the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX). By transitioning legacy wholesale payment ecosystems to Kinexys—which records billions in daily volume—and establishing connectivity with consumer rails like Mastercard, the barriers between isolated permissioned bank ledgers and public layer-1 protocols are decreasing.

Architectural Comparison: Legacy vs. Combined DLT Settlement

To appreciate the structural advantages demonstrated in this pilot, it is necessary to compare the operational components against traditional correspondent banking frameworks:

| Operational Metric | Legacy Correspondent Banking | Combined DLT Settlement Framework (XRPL/MTN/Kinexys) |

| Asset Leg Settlement | Manual brokerage settlement, ledger adjustments via custodians (T+1 to T+2) | Automated smart contract redemption on XRPL ($<5$ seconds) |

| Fiat Leg Execution | SWIFT messaging routed through multiple intermediary clearing houses | Direct ledger integration via Mastercard MTN to J.P. Morgan Kinexys |

| Operational Windows | Restrained by local banking hours and Fedwire cut-off times | Continuous 24/7/365 execution, including weekends and holidays |

| Counterparty Exposure | Prolonged risk during transit across intermediary ledgers | Minimized due to atomic-style automated leg handovers |

| Reconciliation Costs | High due to disparate, un-synchronized ledger systems | Near-zero due to cryptographically verified transaction states |

Pro Tip: The Liquidity Imbalance Matrix

Corporate treasurers evaluating real-world tokenized assets must verify that their chosen token issuer maintains automated API integrations with an interbank network. If an asset tokenizes on a public chain but relies on manual wire transfers for the payout leg, the platform’s capital efficiency degrades, leaving the fund exposed to identical legacy settlement frictions during periods of high volatility.

Risk Profile and Technical Limitations

While the technical execution of this pilot represents an advancement, institutional scale adoption requires analyzing the underlying technical limitations and operational vulnerabilities.

Systemic Smart Contract and Interoperability Risks

The framework relies on the programmatic handoff of data between three distinct environments: the public XRPL, Mastercard’s permissioned messaging infrastructure, and J.P. Morgan’s internal Kinexys ledger. Every integration point represents an abstraction layer that depends on oracle networks or APIs. A software bug, synchronization delay, or data validation failure within Mastercard’s MTN could stall the transaction midway, triggering liquidity mismatches where an asset is burned on-chain but the corresponding bank account fails to credit.

Regulatory Fragmentation Across Jurisdictions

The pilot executed a settlement ending in Singapore using a New York-regulated stablecoin (RLUSD) and a U.S. bank infrastructure. However, the legal definition of finality for transactions executed on public ledgers remains fragmented globally. Should a counterparty face insolvency midway through an international settlement cycle, the legal priority of an on-chain token burn relative to a traditional bankruptcy freeze varies significantly across North American, European, and Asian jurisdictions.

Liquidity Fragmentation in Stablecoin Reserves

For these models to scale, the stablecoin wrappers used on public ledgers must feature deep, institutional-grade secondary liquidity. If redemptions scale to hundreds of millions per transaction, the underlying primary issuance funds (such as BlackRock’s BUIDL or cash equivalents) must establish instant liquidation agreements with primary dealers to prevent delay matching the sub-five-second public ledger execution timeline.

Strategic Future Outlook: The Multichain Wholesale Landscape

The success of these institutional pilots points toward a structural shift in how global liquidity will be organized. We are transitioning away from separate, isolated asset blockchains and moving toward a layered model where public blockchains function as asset issuance networks, while bank-led consortia act as the automated, cross-border clearing engines.

+------------------------------------------------------------------------+

| FUTURE MULTICHAIN ARCHITECTURE |

+------------------------------------------------------------------------+

| |

| [ ISSUANCE LAYER ] Public L1s (XRPL, Ethereum, Avalanche) |

| | |

| v |

| [ INTEROP LAYER ] Programmable Networks (Mastercard MTN, Swift) |

| | |

| v |

| [ SETTLEMENT LAYER ] Wholesale Bank Rail Node Networks (Kinexys) |

| |

+------------------------------------------------------------------------+

As corporate cash allocations migrate into tokenized instruments to capture real-time yields, financial institutions that fail to integrate public ledger access into their core transaction systems risk losing processing volume to networks that can guarantee sub-five-second transaction confirmation.

FAQ SECTION

– What is the primary takeaway from the institutional spotlights on XRPL cross-border settlement utilities?

- The primary takeaway is the successful integration of public blockchain assets with legacy banking rails to achieve a cross-border asset redemption in under five seconds. The pilot demonstrates that public infrastructure like the XRPL can securely interact with institutional bank environments like J.P. Morgan’s Kinexys via interoperability layers like Mastercard’s Multi-Token Network.

– How does the dual-leg settlement problem affect institutional digital asset adoption?

- The dual-leg settlement problem occurs when the asset leg of a transaction finalizes instantly on a blockchain, but the corresponding cash or fiat payout requires days to settle via traditional banking systems. This mismatch introduces operational risk and reduces capital efficiency for institutions managing real-world assets.

– What role did Ripple’s RLUSD stablecoin play in this transaction pilot?

- RLUSD served as the stablecoin instrument for the initial public blockchain leg on the XRP Ledger. Because it is regulated by the New York State Department of Financial Services (NY DFS), it provides a compliant, non-volatile asset wrapper that large institutions can utilize for on-chain settlement without exposure to price volatility.

– What is the purpose of the Mastercard Multi-Token Network (MTN) within this infrastructure?

- The Mastercard Multi-Token Network operates as an intermediate interoperability and messaging layer. It reads the tokenized redemption confirmation from the public blockchain, validates the data, and securely transmits automated payout instructions to private wholesale banking platforms like Kinexys by J.P. Morgan.

– Can this cross-border settlement framework operate outside normal banking hours?

- Yes. The May 2026 pilot proved that the combined integration of XRPL, Mastercard MTN, and Kinexys functions completely outside standard banking hours, allowing corporate treasuries to execute redemptions and settle fiat currency across international borders during weekends and holidays.

FINANCIAL DISCLAIMER

This article is provided strictly for informational and educational purposes. It does not constitute investment, financial, legal, or tax advice. Tokenized real-world assets, stablecoins, and digital ledger technologies involve unique systemic, smart contract, and regulatory risks that can result in capital loss. Readers should conduct individual due diligence and consult with certified financial advisors and legal counsel before committing capital to asset tokenization ecosystems or digital assets.